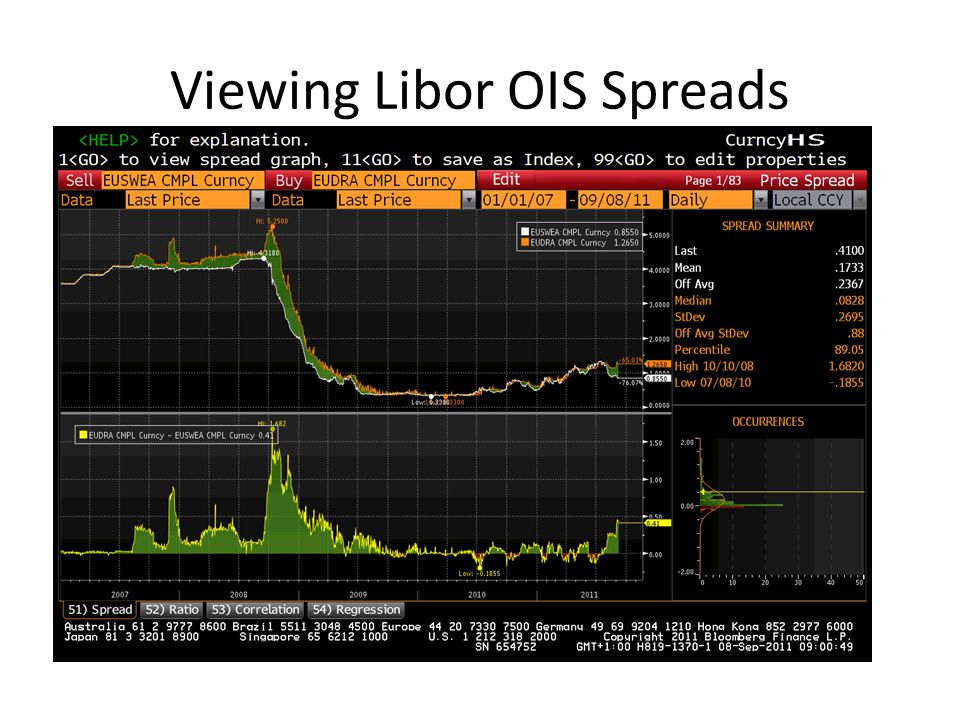

3 Bar chart view of swap spread 1In this section you will explore and analyze the current and historical cross currency basis swap spread for a single currency in XCCY. Van 800u tm 2200u NL tijd.

Movements In The Term Structure Of Interest Rate Source Bloomberg Download Scientific Diagram

It represents the mid-price for interest rate swaps the fixed leg at particular times of the day in three major currencies EUR GBP and USD and in tenors ranging from 1 year to 30 years.

3 year euro swap rate bloomberg. Index performance for Bloomberg AusBond Swap 3 Year Index BASW3 including value chart profile other market data. The 3 month euro EUR LIBOR interest rate is the average interest rate at which a selection of banks in London are prepared to lend to one another in euros with a maturity of 3 months. EUR to NOK Exchange Rate - Bloomberg Markets.

Euro area 3-year Government Benchmark bond yield - Yield Euro area changing composition - Benchmark bond - Euro area 3-year Government Benchmark bond yield - Yield - Euro provided by ECB. Corporate Financial Value Chain. De koersen zijn overal in Euros ook die voor aandelen uit de US en het VK.

For example if we choose a 7-year swap contract it will carry a rate of 22195 as shown in Exhibit 3. The setting will be a 5 Year USD-EUR basis swap spread against the USD Libor rate. 1 Week1 Month1 Year3 Years.

Euro 10 yr Swapindex chart prices and performance plus recent news and analysis. 1 2 180-189 Journal of Bond Trading Management 181 Use of the Bloomberg system in swaps analysis Figure 1 IRSB Bloombergs live swap rate screen Figure 2 GP Bloombergs graph of the historical variations of the five year swap rate. EURO EUR Spot Rate - Bloomberg Markets.

Alongside the 3 month euro EUR LIBOR interest rate we also have a large number of other LIBOR interest rates for other maturities andor in other currencies. Get this FREE widget for your website. The curve Bloomberg EUR swaps curve YCSW0045 Index is indeed the euro equivalent of the Bloomberg USD swaps curve YCSW0023 Index.

Of course we can compute the risk of the swap by using the same method as we employed for the banks balance sheet observing that a pay-fixed-receive floating swap is. Henry Stewart Publications 1476-1688 2002 Vol. ICE Swap Rate is used as the exercise value for cash-settled swaptions for close-out payments on early terminations of interest rate swaps for some floating rate bonds and for valuing portfolios of interest rate swaps.

Dollar risk will be determined by the characteristics of that swap. 5 Years Yield Curve. By equivalent I mean that each curves are constructed in the same manner.

The lastest in Interest rate swap news LIBOR and swap rates. 3 year euro swap rate bloomberg calculation and publication happens in six runs covering four times of the day. Rates Bonds - Bloomberg.

ICE Swap Rate is calculated and published in three currencies EUR GBP and USD with tenors ranging from 1 year to 30 years. 1 Week 1 Month 1 Year 3 Years. Five-year euro interest-rate swaps are outperforming surrounding maturities as the debt proves to be the focal point of rising investor expectations for.

Using sames types of instruments deposits FRAs futures swaps with the same bootstrappingimplying method exact fit vs best fit. Type XCCY in the command line click on Views on.

Introduction To Bloomberg Fx Functions Datapoints A Blog From The Lippincott Library Of The Wharton School Of Business

Pricing And Valuing Interest Rate Swaps On Bloomberg Ppt Download